Taxability of Transactions in Shares, Securities and Derivatives

- Gopinathan Associates

- Oct 16, 2019

- 3 min read

Updated: Oct 17, 2019

SMRITHI SURESH BABU

ACA, B.com

The trading in shares, securities and derivatives is gaining more and more significance in current economic scenario due to its high earning potential, sharing of risk, arbitrage opportunities and also protection against fluctuations in price as compared to the traditional investment alternatives.

The purchase or sale of stocks and shares undertaken by the assessee may be in the course of business or for the purpose of investment. This is a judgement call and will depend on the facts and circumstances of each case such as nature, frequency, and volume of transaction.

The following judgments can be referred to for deciding the nature of transaction:

In case it is concluded that the transactions are for the purposes of investment and profit/loss arising there from is to be assessed under the head 'Capital Gains. However, in case such transactions are in the course of business, then the profit/ loss arising there from shall be assessed under the head ‘Profit or gains from business or profession’.

As per section 44AB tax audit is applicable for:

1) Any person pursuing business and whose total turnover or gross receipts exceed a sum of 1 crore rupees in any previous year (N.A applicable to the persons who opts for presumptive taxation scheme).

2) Any person pursuing profession and whose gross profits exceed fifty lakh rupees in any previous year.

3) A person who is considered eligible for the presumptive taxation scheme, and who claims that the profits and gains for the respective business is lower than what is computed in accordance with the presumptive taxation scheme and his/her income exceeds the amount that is taxable. This provision is applicable to the taxpayers who opt for presumptive taxation scheme other than the one who choose the scheme under Section 44AD and whose sale or turnover is limited to Rs 2 crores.

Here comes the question of How to calculate this turnover in the case of shares and securities when considering it as a business income.

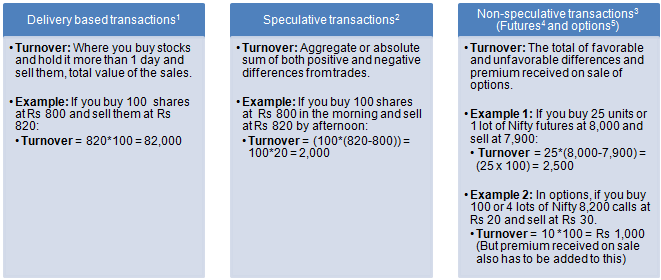

The method of calculating turnover is a debatable issue and what makes it a grey area is that there is no guideline as such from the IT department. One article of great help though is the Guidance Note on tax audit under Section 44AB by ICAI (Institute of Chartered accountants of India). Section 5.12 of the guidance note provides the methodology for computation of turnover in such cases:

The turnover can be calculated scrip wise or trade wise.

Conclusion

In case of assesses trading in shares and derivatives, it is likely that they have a turnover more than 1 Cr or they have turnover less than 2 Cr but have a loss or profit less than 6% on such turnover. In both such cases tax audit shall be applicable to such persons as discussed above.

Disclaimer

All content on the site and all services provided through it are provided without any guarantees of completeness, accuracy or timeliness, and without representations, warranties or other contractual terms of any kind, express or implied.

Gopinathan Associates does not represent or warrant that this site, the various services provided through this site, and / or any information, software or other material downloaded from this site, will be accurate, current, uninterrupted, error-free, omission-free or free of viruses or other harmful components.

The information presented on this site should not be construed as legal, tax, accounting or any other professional advice or service. You should consult with qualified Chartered Accountant or professional advisor for familiar with your particular factual situation for advice concerning specific tax or other matters before making any decision. You should not send any confidential information to our firm until you have received agreement from the firm to perform the services you request.

Dealing in shares can result either in "Business income" (u/s 28 of the Income Tax Act, 1961) or "Capital Gains" (u/s.45 of the Act) is a hot topic always. Classification into Business Income and Capital Gains depends on facts & circumstances of each case and it has been well explained in the above discussion. Good work Smrithi. Keep doing well.